Our Tap-and-Go Lifestyles are Putting the Financial Screws In

Our Tap-and-Go Lifestyles are Putting the Financial Screws In

How Convenience is Costing Us

What a time to be alive!

The world is at our fingertips, a cornucopia of convenience available with a tap of a button. Hungry? Grab Food (Asia’s Uber Eats) will deliver meals or groceries to your door in a matter of minutes. Need a new dog lead? Amazon Prime will have it with you by tomorrow. Feeling bored? Endless entertainment awaits on Netflix, Hulu, or through gaming service subscriptions. Bills are paid automatically through direct debit and we metaphorically fly through our commutes with a simple tap of our cards or the backs of our phones.

We’re in a consumer’s paradise, aren’t we? But at what cost?

Hands up (or, better yet, give this article a thumbs up) if you’ve ever checked your bank account and been absolutely floored by the amount of debits taken from your card. How many times have you scrolled through your bank statement trying to place all the micro-transactions to a specific purchase or event, but not been able to link it? Two? Five? A dozen times every month, maybe?

The truth is that the instant gratification lifestyle comes at a sizeable cost and when all things are said and done, our bank accounts look like they’ve been through the shredder.

“How much do you think you spend on takeouts and casual shopping each month?”, I ask my clients.

“Can’t be more than $500”, they say. (Arbitrary figure - everyone is completely different.)

But from personal experience, and unless the individual in question keeps track of their expenses with a budget, 9 times out of 10 the person I speak to will have underestimated just how much money they spend.

You see, the beauty of the cashless society has a dark side. It wreaks havoc on our concept of spending and the undercurrent of small costs completely decimates any notion of financial control.

Then what are we to do?

Look, in today’s day and age, there is absolutely no way that we’re going to escape the tap-and-go trap. Unless you live here in Vietnam or in other countries where cash still circulates in abundance, there’s just no way to avoid the cashless surge.

The good news is, you're not powerless! We can declutter our spending before it even begins. I touched upon it last week in The Great Financial Caffeine Catastrophe, but by taking a more mindful approach to our spending, we can break free from the anxiety of these incessant micro expenses.

Pay Yourself First

Budgeting is boring, time-consuming and restrictive, right? Dave Ramsey (a US personal finance personality) loves to say that you should give every dollar or dong you earn a job. Dave Ramsey isn’t necessarily wrong but zero-based budgeting, which his advice is also known as, is very hard to stick to.

Instead, I would recommend to try and pay yourself first. My frequent readers will roll their eyes, knowing that I preach this daily but it’s because it works. As soon as your income hits your account, immediately transfer a specific percent into savings and/or investments. It doesn’t matter if it’s 5% or 20%, start low and work your way up.

Once you know that you’re taking care of your financial future it won’t matter how many micro transactions appear on your bank statement. You’ll use the money you have left in your account throughout the rest of the month like normal and hopefully, instinctively, not use more than you have.

Understand that most of us aren’t terrible when it comes to handling our money, we just lack strategy.

What do I do?

I do a bit of both.

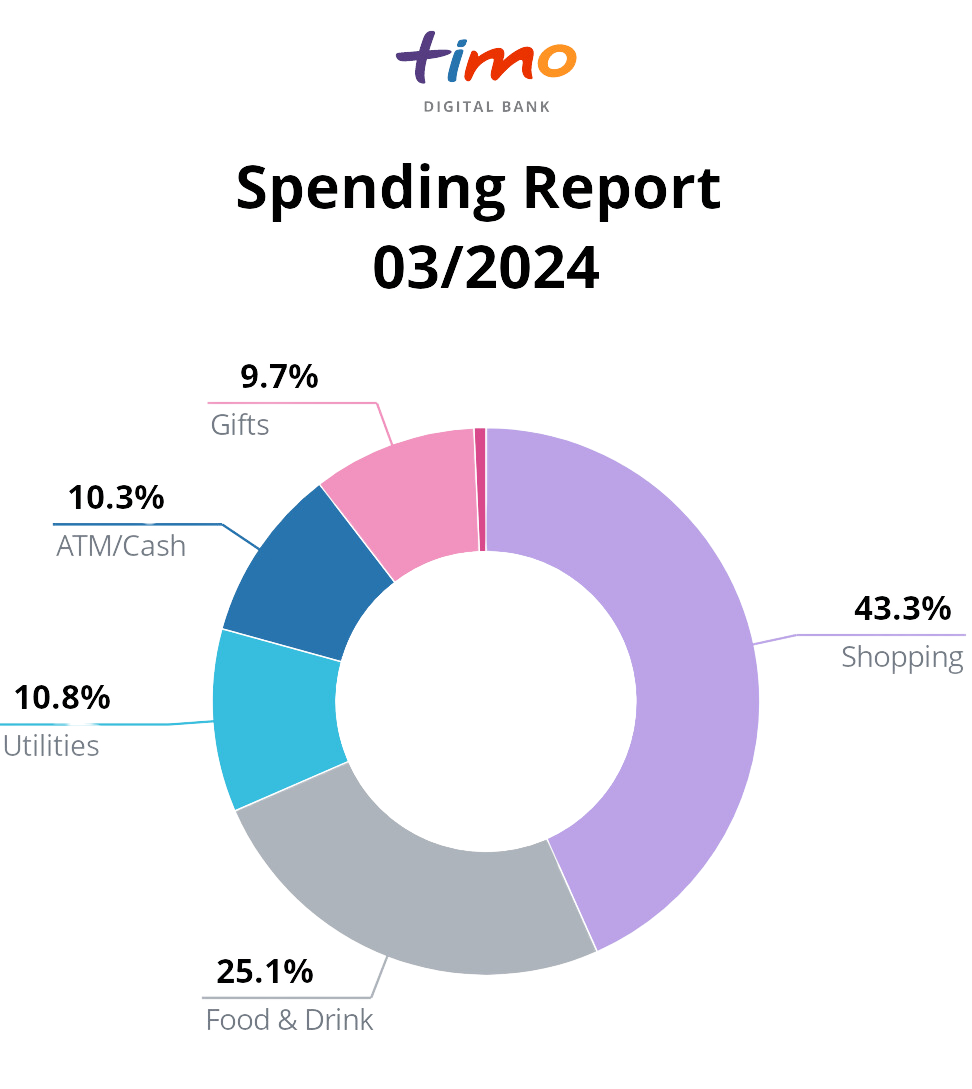

Like most, I hate budgeting. Thankfully these new fintech banks are amazing and often keep track of your spending for you. Currently, I use Revolut and Timo (in Vietnam).

Every month my bank will give me a lovely little breakdown of my spending. Any day of the week I can review my pie chart and quickly see in what category I spend my money. If I feel like I’m overspending in any given area, I can regulate myself for the rest of the month. Look at this beauty.

Additionally, I pay myself first. With a fluctuating income, I can’t invest a specific $ sum every month so I simply invest a % of my take home. Every little helps and this ensures that I am still prioritising my future above all else.

Like it, love it, hate it? Drop me a comment or a question!

Remember, you owe me a thumbs up if you’ve ever been shocked by the amount of ‘micro’ transactions in your bank statement!

OK, I have to ask. What counts as "Shopping" that it takes up a whopping 43%? I see "Shopping" and I think clothes. But surely you can't be buying that much clothes. 😆